Free CFA Institute CFA-Level-III Exam Questions

Absolute Free CFA-Level-III Exam Practice for Comprehensive Preparation

Page No. 1 of 73

-

Question 1

-

Gabrielle Reneau, CFA, and Jack Belanger specialize in options strategies at the brokerage firm of Damon andDamon. They employ fairly sophisticated strategies to construct positions with limited risk, to profit from futurevolatility estimates, and to exploit arbitrage opportunities. Damon and Damon also provide advice to outsideportfolio managers on the appropriate use of options strategies. Damon and Damon prefer to use, andrecommend, options written on widely traded indices such as the S&P 500 due to their higher liquidity.However, they also use options written on individual stocks when the investor has a position in the underlyingstock or when mispricing and/or trading depth exists.In order to trade in the one-year maturity puts and calls for the S&P 500 stock index, Reneau and Belangercontact the chief economists at Damon and Damon, Mark Blair and Fran Robinson. Blair recently joined Damonand Damon after a successful stint at a London investment bank. Robinson has been with Damon and Damonfor the past ten years and has a considerable record of success in forecasting macroeconomic activity. In hisforecasts for the U.S. economy over the next year, Blair is quite bullish, for both the U.S. economy and the S&P500 stock index. Blair believes that the U.S. economy will grow at 2% more than expected over the next year.He also states that labor productivity will be higher than expected, given increased productivity through the useof technological advances. He expects that these technological advances will result in higher earnings for U.S.firms over the next year and over the long run.Reneau believes that the best S&P 500 option strategy to exploit Blair's forecast involves two options of thesame maturity, one with a low exercise price, and the other with a high exercise price. The beginning stockprice is usually below the two option strike prices. She states that the benefit of this strategy is that themaximum loss is limited to the difference between the two option prices.Belanger is unsure that Blair's forecast is correct. He states that his own reading of the economy is for acontinued holding pattern of low growth, with a similar projection for the stock market as a whole. He states thatDamon and Damon may want to pursue an options strategy where a put and call of the same maturity andsame exercise price are purchased. He asserts that such a strategy would have losses limited to the total costof the two options.Reneau and Belanger are also currently examining various positions in the options of Brendan Industries.Brendan Industries is a large-cap manufacturing firm with headquarters in the midwestern United States. Thefirm has both puts and calls sold on the Chicago Board Options Exchange. Their options have good liquidity forthe near money puts and calls and for those puts and calls with maturities less than four months. Reneaubelieves that Brendan Industries will benefit from the economic expansion forecasted by Mark Blair, the Damonand Damon economist. She decides that the best option strategy to exploit these expectations is for her topursue the same strategy she has delineated for the market as a whole.Shares of Brendan Industries are currently trading at $38. The following are the prices for their exchangetraded options.

As a mature firm in a mature industry, Brendan Industries stock has historically had low volatility. However,Belanger's analysis indicates that with a lawsuit pending against Brendan Industries, the volatility of the stockprice over the next 60 days is greater by several orders of magnitude than the implied volatility of the options.He believes that Damon and Damon should attempt to exploit this projected increase in Brendan Industries1volatility by using an options strategy where a put and call of the same maturity and same exercise price areutilized. He advocates using the least expensive strategy possible.During their discussions, Reneau cites a counter example to Brendan Industries from last year. She recalls thatNano Networks, a technology firm, had a stock price that stayed fairly stable despite expectations to thecontrary. In this case, she utilized an options strategy where three different calls were used. Profits were earnedon the strategy because Nano Networks' stock price stayed fairly stable. Even if the stock price had becomevolatile, losses would have been limited.Later that week, Reneau and Belanger discuss various credit option strategies during a lunch time presentationto Damon and Damon client portfolio managers. During their discussion, Reneau describes a credit optionstrategy that pays the holder a fixed sum, which is agreed upon when the option is written, and occurs in theevent that an issue or issuer goes into default. Reneau declares that this strategy can take the form of eitherputs or calls. Belanger states that this strategy is known as either a credit spread call option strategy or a creditspread put option strategy.Reneau and Belanger continue by discussing the benefits of using credit options. Reneau mentions that creditoptions written on an underlying asset will protect against declines in asset valuation. Belanger says that creditspread options protect against adverse movements of the credit spread over a referenced benchmark.Assume Reneau applies the options strategy used earlier for Nano Networks. Assuming there is a 3-month 45call on Brendan Industries trading at $1.00, calculate the maximum gain and maximum loss on this position.Max gain Max loss

As a mature firm in a mature industry, Brendan Industries stock has historically had low volatility. However,Belanger's analysis indicates that with a lawsuit pending against Brendan Industries, the volatility of the stockprice over the next 60 days is greater by several orders of magnitude than the implied volatility of the options.He believes that Damon and Damon should attempt to exploit this projected increase in Brendan Industries1volatility by using an options strategy where a put and call of the same maturity and same exercise price areutilized. He advocates using the least expensive strategy possible.During their discussions, Reneau cites a counter example to Brendan Industries from last year. She recalls thatNano Networks, a technology firm, had a stock price that stayed fairly stable despite expectations to thecontrary. In this case, she utilized an options strategy where three different calls were used. Profits were earnedon the strategy because Nano Networks' stock price stayed fairly stable. Even if the stock price had becomevolatile, losses would have been limited.Later that week, Reneau and Belanger discuss various credit option strategies during a lunch time presentationto Damon and Damon client portfolio managers. During their discussion, Reneau describes a credit optionstrategy that pays the holder a fixed sum, which is agreed upon when the option is written, and occurs in theevent that an issue or issuer goes into default. Reneau declares that this strategy can take the form of eitherputs or calls. Belanger states that this strategy is known as either a credit spread call option strategy or a creditspread put option strategy.Reneau and Belanger continue by discussing the benefits of using credit options. Reneau mentions that creditoptions written on an underlying asset will protect against declines in asset valuation. Belanger says that creditspread options protect against adverse movements of the credit spread over a referenced benchmark.Assume Reneau applies the options strategy used earlier for Nano Networks. Assuming there is a 3-month 45call on Brendan Industries trading at $1.00, calculate the maximum gain and maximum loss on this position.Max gain Max loss

Answer: A

-

-

Question 2

-

Carl Cramer is a recent hire at Derivatives Specialists Inc. (DSI), a small consulting firm that advises a varietyof institutions on the management of credit risk. Some of DSI's clients are very familiar with risk managementtechniques whereas others are not. Cramer has been assigned the task of creating a handbook on credit risk,its possible impact, and its management. His immediate supervisor, Christine McNally, will assist Cramer in thecreation of the handbook and will review it. Before she took a position at DSI, McNally advised banks and otherinstitutions on the use of value-at-risk (VAR) as well as credit-at-risk (CAR).Cramer's first task is to address the basic dimensions of credit risk. He states that the first dimension of creditrisk is the probability of an event that will cause a loss. The second dimension of credit risk is the amount lost,which is a function of the dollar amount recovered when a loss event occurs. Cramer recalls the considerabledifficulty he faced when transacting with Johnson Associates, a firm which defaulted on a contract with theGrich Company. Grich forced Johnson Associates into bankruptcy and Johnson Associates was declared indefault of all its agreements. Unfortunately, DSI then had to wait until the bankruptcy court decided on all claimsbefore it could settle the agreement with Johnson Associates.McNally mentions that Cramer should include a statement about the time dimension of credit risk. She statesthat the two primary time dimensions of credit risk are current and future. Current credit risk relates to thepossibility of default on current obligations, while future credit risk relates to potential default on futureobligations. If a borrower defaults and claims bankruptcy, a creditor can file claims representing the face valueof current obligations and the present value of future obligations. Cramer adds that combining current andpotential credit risk analysis provides the firm's total credit risk exposure and that current credit risk is usually areliable predictor of a borrower's potential credit risk.As DSI has clients with a variety of forward contracts, Cramer then addresses the credit risks associated withforward agreements. Cramer states that long forward contracts gain in value when the market price of theunderlying increases above the contract price. McNally encourages Cramer to include an example of credit riskand forward contracts in the handbook. She offers the following:A forward contract sold by Palmer Securities has six months until the delivery date and a contract price of 50.The underlying asset has no cash flows or storage costs and is currently priced at 50. In the contract, no fundswere exchanged upfront.Cramer also describes how a client firm of DSI can control the credit risks in their derivatives transactions. Hewrites that firms can make use of netting arrangements, create a special purpose vehicle, require collateralfrom counterparties, and require a mark-to-market provision. McNally adds that Cramer should include adiscussion of some newer forms of credit protection in his handbook. McNally thinks credit derivativesrepresent an opportunity for DSL She believes that one type of credit derivative that should figure prominently intheir handbook is total return swaps. She asserts that to purchase protection through a total return swap, theholder of a credit asset will agree to pass the total return on the asset to the protection seller (e.g., a swapdealer) in exchange for a single, fixed payment representing the discounted present value of expected cashflows from the asset.A DSI client, Weaver Trading, has a bond that they are concerned will increase in credit risk. Weaver would likeprotection against this event in the form of a payment if the bond's yield spread increases beyond LIBOR plus3%. Weaver Trading prefers a cash settlement.Later that week, Cramer and McNally visit a client's headquarters and discuss the potential hedge of a bondissued by Cuellar Motors. Cuellar manufactures and markets specialty luxury motorcycles. The client isconsidering hedging the bond using a credit spread forward, because he is concerned that a downturn in theeconomy could result in a default on the Cuellar bond. The client holds $2,000,000 in par of the Cuellar bondand the bond's coupons are paid annually. The bond's current spread over the U.S. Treasury rate is 2.5%. Thecharacteristics of the forward contract are shown below.Information on the Credit Spread Forward

Determine whether the forward contracts sold by Palmer Securities have current and/or potential credit risk.

Determine whether the forward contracts sold by Palmer Securities have current and/or potential credit risk.

Answer: B

-

-

Question 3

-

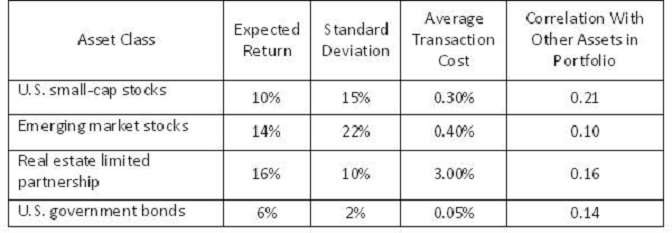

Dan Draper, CFA is a portfolio manager at Madison Securities. Draper is analyzing several portfolios whichhave just been assigned to him. In each case, there is a clear statement of portfolio objectives and constraints,as welt as an initial strategic asset allocation. However, Draper has found that all of the portfolios haveexperienced changes in asset values. As a result, the current allocations have drifted away from the initialallocation. Draper is considering various rebalancing strategies that would keep the portfolios in line with theirproposed asset allocation targets.Draper spoke to Peter Sterling, a colleague at Madison, about calendar rebalancing. During their conversation,Sterling made the following comments:Comment 1: Calendar rebalancing will be most efficient when the rebalancing frequency considers the volatilityof the asset classes in the portfolio.Comment 2: Calendar rebalancing on an annual basis will typically minimize market impact relative to morefrequent rebalancing.Draper believes that a percentage-of-portfolio rebalancing strategy will be preferable to calendar rebalancing,but he is uncertain as to how to set the corridor widths to trigger rebalancing for each asset class. As anexample, Draper is evaluating the Rogers Corp. pension plan, whose portfolio is described in Figure 1.

Draper has been reviewing Madison files on four high net worth individuals, each of whom has a $1 millionportfolio. He hopes to gain insight as to appropriate rebalancing strategies for these clients. His research so farshows:Client A is 60 years old, and wants to be sure of having at least $800,000 upon his retirement. His risk tolerancedrops dramatically whenever his portfolio declines in value. He agrees with the Madison stock market outlook,which is for a long-term bull market with few reversals.Client B is 35 years old and wants to hold stocks regardless of the value of her portfolio. She also agrees withthe Madison stock market outlook.Client C is 40 years old, and her absolute risk tolerance varies proportionately with the value of her portfolio.She does not agree with the Madison stock market outlook, but expects a choppy stock market, marked bynumerous reversals, over the coming months.In selecting a rebalancing strategy for his clients, Draper would most likely select a constant mix strategy for:

Draper has been reviewing Madison files on four high net worth individuals, each of whom has a $1 millionportfolio. He hopes to gain insight as to appropriate rebalancing strategies for these clients. His research so farshows:Client A is 60 years old, and wants to be sure of having at least $800,000 upon his retirement. His risk tolerancedrops dramatically whenever his portfolio declines in value. He agrees with the Madison stock market outlook,which is for a long-term bull market with few reversals.Client B is 35 years old and wants to hold stocks regardless of the value of her portfolio. She also agrees withthe Madison stock market outlook.Client C is 40 years old, and her absolute risk tolerance varies proportionately with the value of her portfolio.She does not agree with the Madison stock market outlook, but expects a choppy stock market, marked bynumerous reversals, over the coming months.In selecting a rebalancing strategy for his clients, Draper would most likely select a constant mix strategy for:

Answer: C

-

- Question 4

- Question 5

PAGE: 1 - 73